.png)

Preparing for an increase in Forms 1099-K

In an era of rapid economic and regulatory change, digital economy businesses (e.g., gig, creator, fin-tech, etc.) and others need to understand and adapt to the continuous rule changes to stay in compliance with tax requirements.

The Form 1099-K is used to report gross amounts of payments that a Payment Settlement Entity (“PSE”) makes to a participating payee, including self-employment earnings and/or proceeds from the sale of personal items.

As part of the American Rescue Plan of 2021, the Form 1099-K reporting thresholds related to third-party network transactions were dramatically reduced to gross payments that exceed $600, regardless of the number of transactions, significantly increasing the number of Forms 1099-K that will be required to be filed.

After temporary relief was provided by the IRS, the reduced threshold is set to go in-effect beginning with the 2023 tax year. Payers should keep their eye on whether additional relief is provided by the IRS, while also being cognizant that certain states have already lowered the reporting threshold at the state-level.

Form 1099-K, is the standardized IRS form utilized to report Payment Card and Third Party Network Transactions. It is the mechanism by which U.S. businesses report information to the IRS in compliance with IRC Section 6050W, which took effect in 2010 with the intention to ensure that online retailers report total sales on their annual tax return.

Specifically, the Form 1099-K reports the gross amount of payments that a PSE makes to a participating payee, including self-employment earnings and/or proceeds from the sale of personal items. Generally these payments are received from the following sources:

Forms 1099-K are due to Recipients by January 31 and to the IRS by March 31, with an optional 30-day automatic extension available for each deadline.

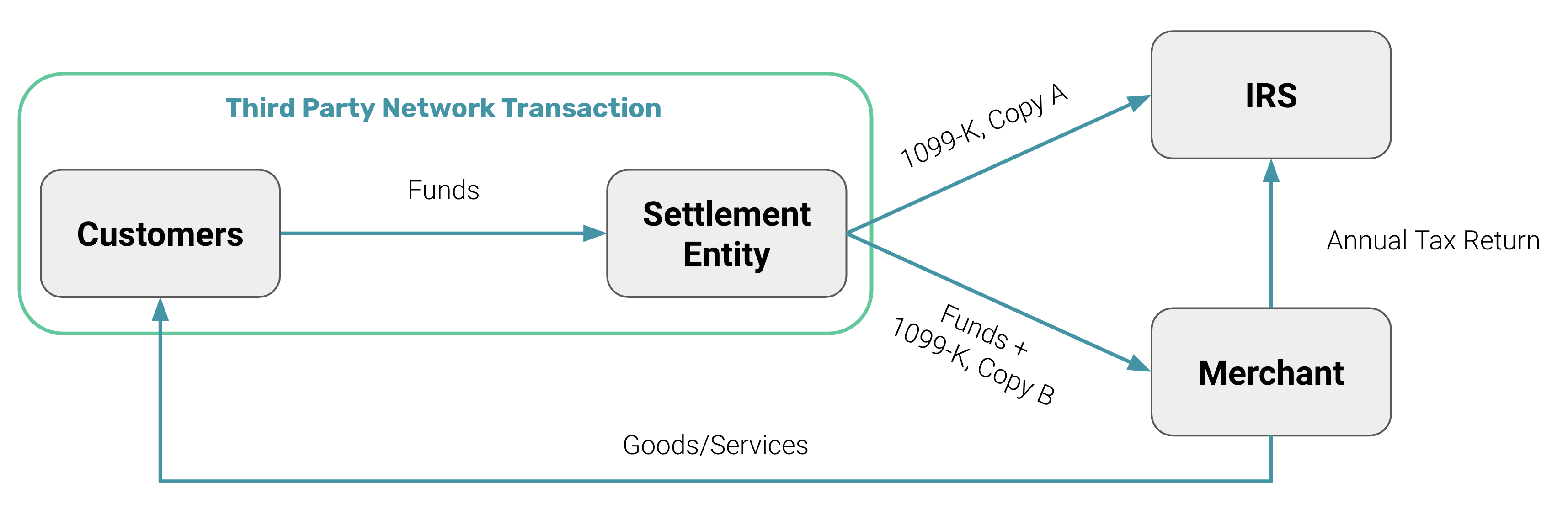

Below is the general structure of a third party network transaction, prompting a Form 1099-K reporting obligation for the Settlement Entity, given the following context – Consider an online auction-payment facilitator, a third-party settlement organization that transfers funds between buyers and sellers (i.e., the Merchant). The payment facilitator is a PSE that is required to report the gross amount paid to each US seller (in this instance, the “payee”) on Form 1099-K, provided certain transaction volume and dollar thresholds are met.

For more details, please visit the IRS website here.

Based on the Section 6050W Regulations released in 2010, a PSE was required to complete Form 1099-K reporting for a given tax year, if a payee meets the following criteria:

As part of the American Rescue Plan of 2021, however, the Form 1099-K reporting thresholds related to third-party network transactions were dramatically reduced to gross payments that exceed $600, regardless of the number of transactions.

The updated criteria will drastically increase the responsibilities of certain U.S. businesses, as it will substantially increase the number of Forms 1099-K that will need to be filed.

This change to the reporting threshold was intended to take effect starting in the 2022 tax season. In December 2022, however, the IRS announced a delay for implementation of a lower threshold until the 2023 tax season. The reason for the delay was to allow businesses time to implement these changes internally to be compliant with these new rules.

It has yet to be seen whether the IRS will extend this relief period. Please note, however, that certain states have already lowered the threshold for gross earnings and have removed the minimum transaction requirement. As such, the lower thresholds will need to be applied for purposes of completing state reporting, regardless of whether additional relief is provided at the federal level.

Taxbit supports the entire tax reporting process in an automated and streamlined manner from Form W-9 collection through Form 1099 reporting.

Simplify your tax compliance with Taxbit. Our modern approach to tax compliance automates information collection and validation from onboarding to form generation, delivery, and filing – enabling you to stay compliant with an ever-changing regulatory landscape.

See our solution in action, request a demo today