.png)

Lower tax liability by accounting for fees.

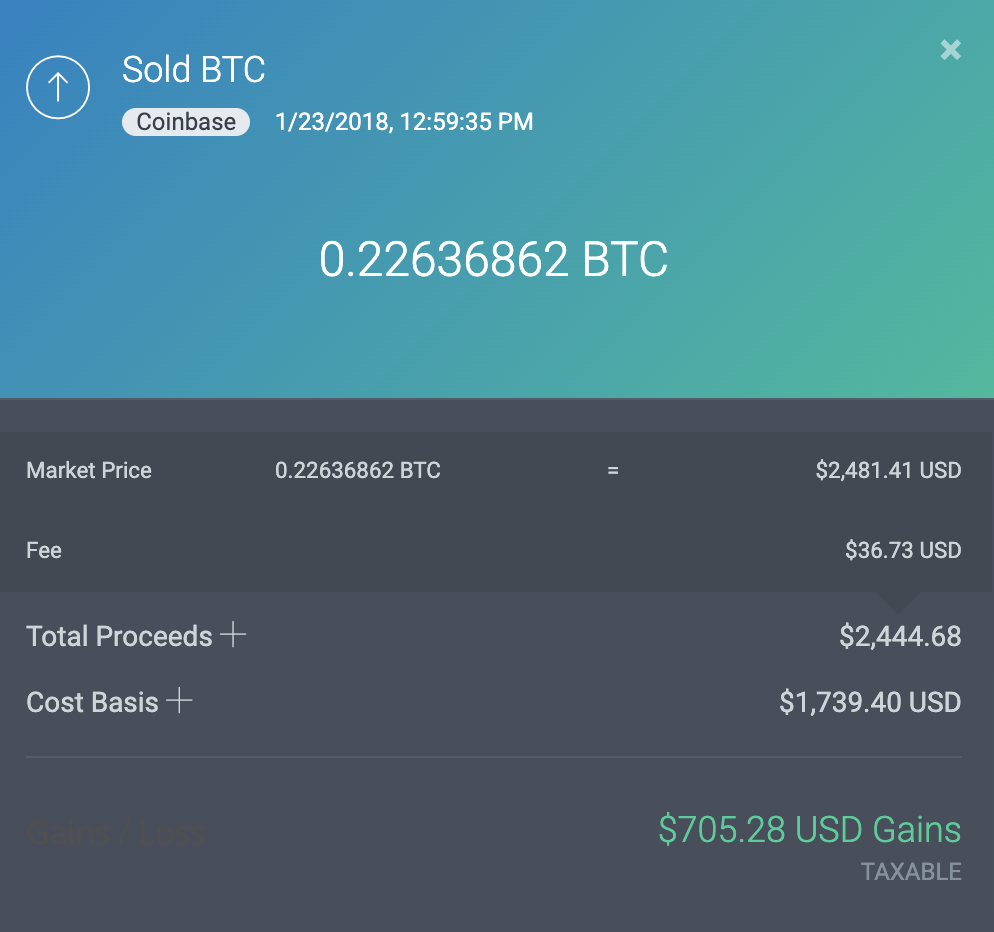

Cryptocurrency exchanges monetize their businesses by charging transaction fees for the acquisition, disposition, or a trade of cryptocurrency. Similar to equity brokers, transaction fees are a necessary evil so that exchanges don’t have to charge monthly or yearly fees to use their services. Whether exchanges monetize through exchange fees, or liquidity spread, TaxBit optimizes to ensure the best results.

Prior to the Tax Cuts and Jobs Act (TCJA) certain investment-related expenses were eligible for itemized deductions. For tax years 2018 to 2025 these deductions have been eliminated. Taxpayer’s, however, can still save money on their transaction fees by adjusting their cost basis on the acquisition of crypto and from deducting fees from the sale proceeds from the disposition of crypto.

TaxBit is here to shed light on how deducting fees operated prior to 2018 and how removing the miscellaneous itemized deduction for investment related expenses after 2018 is actually not a very big deal for the vast majority of crypto traders because adjusting cost basis and proceeds amounts is typically more tax beneficial than the prior itemized deduction.

Misc. Itemized Deductions on Investment Expenses

Prior to 2018, taxpayers had the option to deduct investment related expenses if they itemize their deductions. The Tax Cuts and Jobs Act of 2017 (TCJA) eliminated this itemized deduction. Although at first glance this may seem unfortunate, the reality is that this won’t impact the vast majority of taxpayers and there are other more beneficial methods of accounting for fees to reduce your tax liability.

As a matter of course, taxpayers must choose when filing their tax return to claim either the standard or itemized deduction. If a taxpayer itemizes their deductions then they will not be eligible for the standard deduction. In 2017 the standard deduction was $6,350 if single or $12,700 if married. The prior investment related expense deduction was only available if the taxpayer chose to itemize their deductions. In 2014, approximately 30 percent of taxpayers chose to itemize their deductions, which would have allowed the taxpayer to deduct investment-related expenses if they had any.

For the 2018 tax year forward, the TCJA nearly doubled the standard deduction to $12,000 for single filers and $24,000 for taxpayers who are married filing jointly. This larger standard deduction highly incentivizes taxpayers to claim the standard deduction. It is projected that 88% of taxpayers that file taxes will now claim the standard deduction. The other 12% who still choose to itemize primarily consists of high wealth individuals. Therefore, eliminating the investment-related deduction for those who itemize now impacts far fewer taxpayers because there is a greater incentive to claim the standard deduction. Importantly, taxpayers had the option of reporting their investment related fees through the itemized deduction, or by applying their fees to their cost basis or proceeds.

Adjusting Cost Basis and Proceeds For Fees

By opting for the standard deduction taxpayers can adjust their cost basis and proceeds amount to account for cryptocurrency exchange fees. Prior to 2018, if taxpayers chose to claim the itemized deduction and deduct cryptocurrency exchange fees, then they would not be eligible to adjust their cost basis for fees. With the investment-related expense itemized deduction eliminated, taxpayers can account for all fees the same way by including them in the acquisition and disposition costs.

If a taxpayer buys cryptocurrency then the acquisition fees can be added to increase their cost basis. Similarly, when a taxpayer sells cryptocurrency they can deduct fees from their proceeds. This is beneficial because it results in lower gains or higher losses.

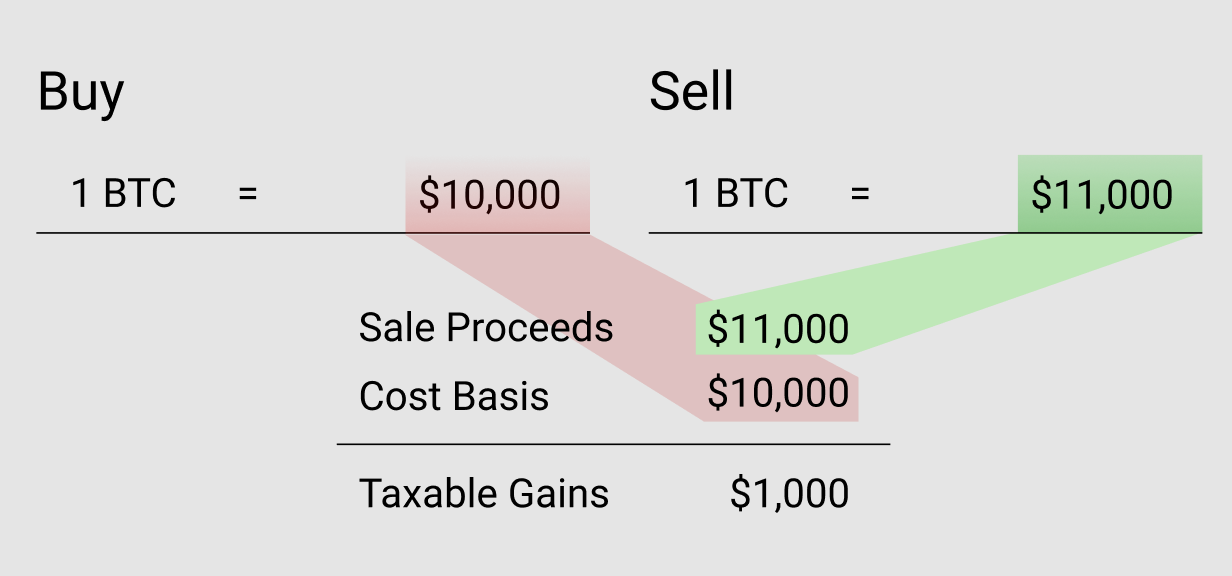

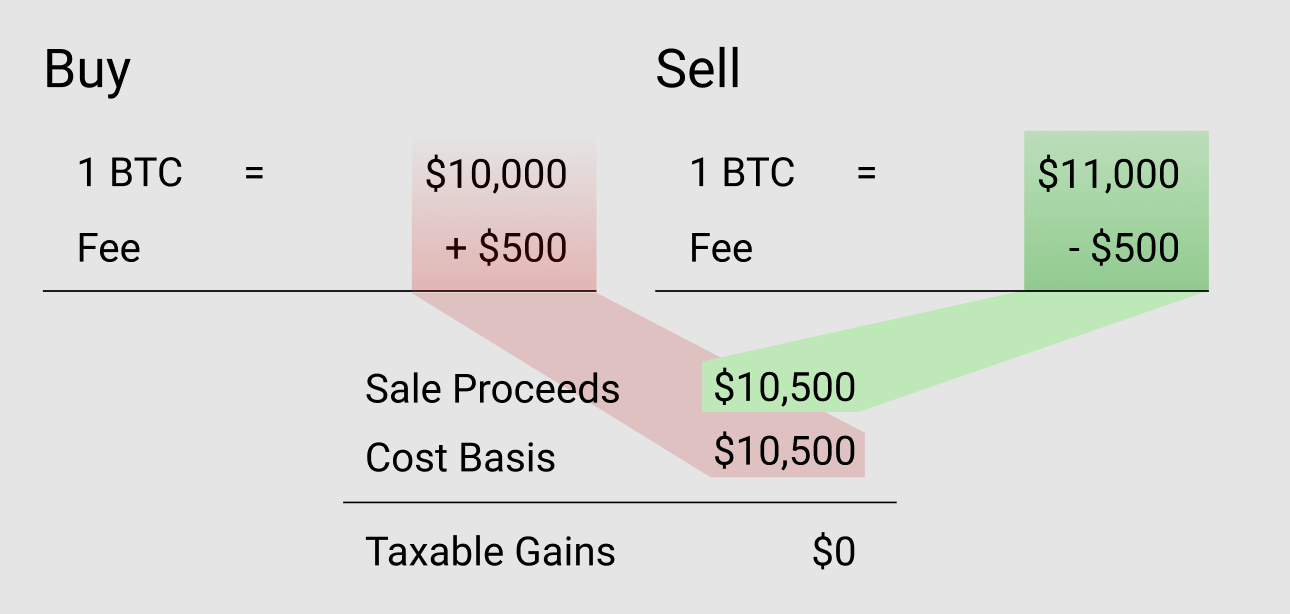

As an example, if a taxpayer buys $10,000 worth of Bitcoin and pays $500 in fees, then the IRS allows you to report a cost basis of $10,500. This ensures that your Bitcoin must go up in value before you realize taxable gains, and if the Bitcoin drops in value then you will realize more losses.

This same example applies inversely for fees from proceeds from selling cryptocurrency. If the taxpayer sells their Bitcoin for $11,000 and pays $500 in fees, then the IRS allows the taxpayer to deduct the $500 from the proceeds. In this example, the taxpayer would report proceeds of $10,500 from selling the crypto.

In the above example, if fees were not accounted for then the taxpayer would have a cost basis of $10,000 in the Bitcoin and proceeds of $11,000. This would result in a $1,000 taxable gain.

However, if fees are accounted for then the taxpayer would have a cost basis of $10,500 and proceeds of $10,500, leaving them with no taxable gains.

Cryptocurrency traders often make hundreds, if not thousands of trades a year. Accounting for fees on every transaction can be nearly impossible to do manually. Fortunately, TaxBit automatically accounts for exchange fees. Exchange fees can quickly add up. TaxBit’s team of tax experts ensure that you maximize your tax savings in a compliant fashion.