.png)

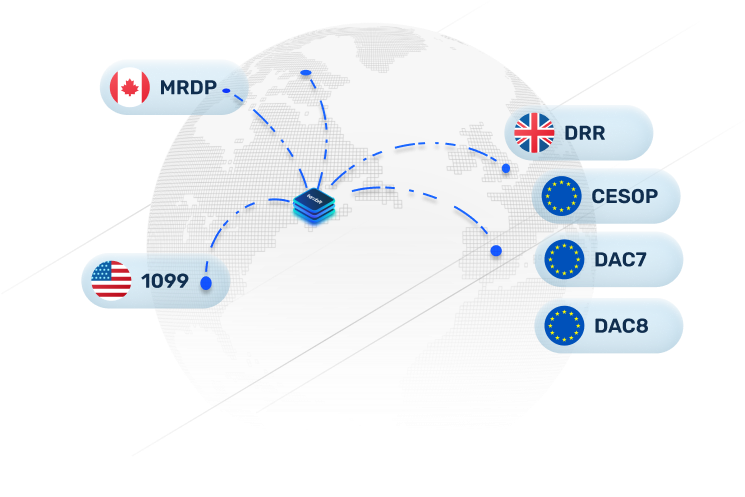

Automate complex, high-volume tax reporting across jurisdictions and currencies. Taxbit simplifies compliance across digital and non-digital assets for seamless global reporting.

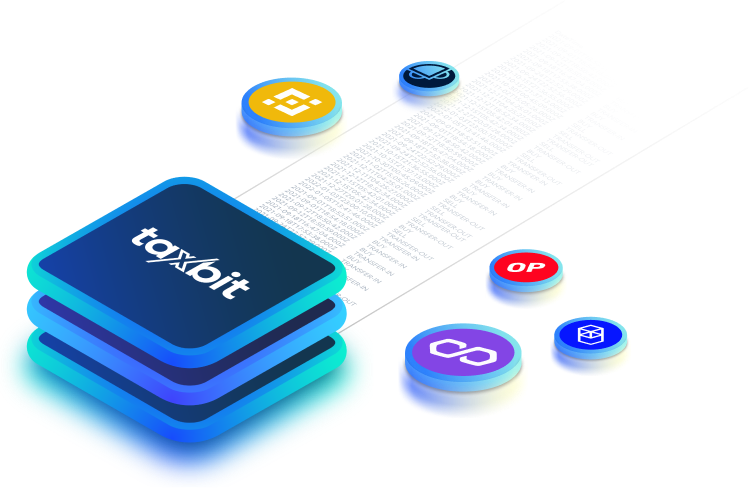

Seamlessly ingest account data from multiple sources, including self-certifications, W-9/W-8 forms, and general account information.

Taxbit consolidates your customer data into a single, unified system for efficient processing and compliance.

Automate the generation and verification of tax forms with precision. Taxbit handles complex calculations and ensures data accuracy at scale.

Effortlessly generate, file, and remediate tax reports across jurisdictions. Taxbit supports seamless submission while enabling compliance with global reporting standards, saving time and reducing manual effort.