.png)

New guidance from the Financial Accounting Standards Board will promote much-needed transparency for companies dealing in digital assets

Key takeaways:

On December 14th, the FASB held a public meeting to vote on issues regarding the presentation of digital assets by public and private companies following US GAAP. The meeting further clarified their October decision to treat crypto holdings at fair value (meaning that assets will be presented according to current market value, and any changes in value will flow through earnings). Currently, digital assets on balance sheets are accounted for at their lowest valuation since the initial point of purchase – requiring impairment analysis to be performed on a regular basis.

As a result of the new vote, companies should present crypto holdings separate from other intangible assets (such as patents or trademarks, or other non-physical assets) on the face of key financial statements. Balance sheets will have a separate line item specifically dedicated to crypto holdings and, as previously determined, those holdings will be reflected at their fair value at the end of the reporting period. Any changes in fair value on income statements will be reflected as a component of net income and broken out as a separate line item.

These presentation decisions will significantly increase financial transparency about the holdings and earnings impact of specific crypto assets – tracking the assets held, the quantity of assets held, and the cost basis and fair value of those assets at the time of the reporting. The FASB’s series of new decisions herald a significant positive change for companies interested in digital assets and for investors seeking greater transparency.

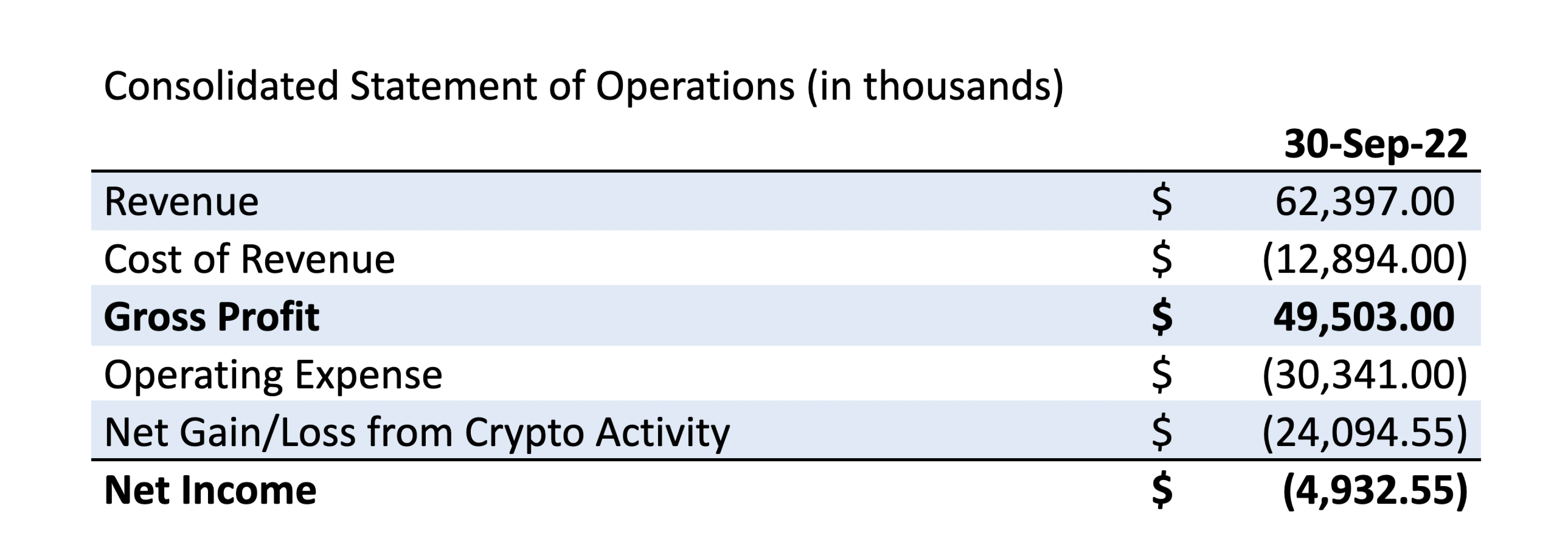

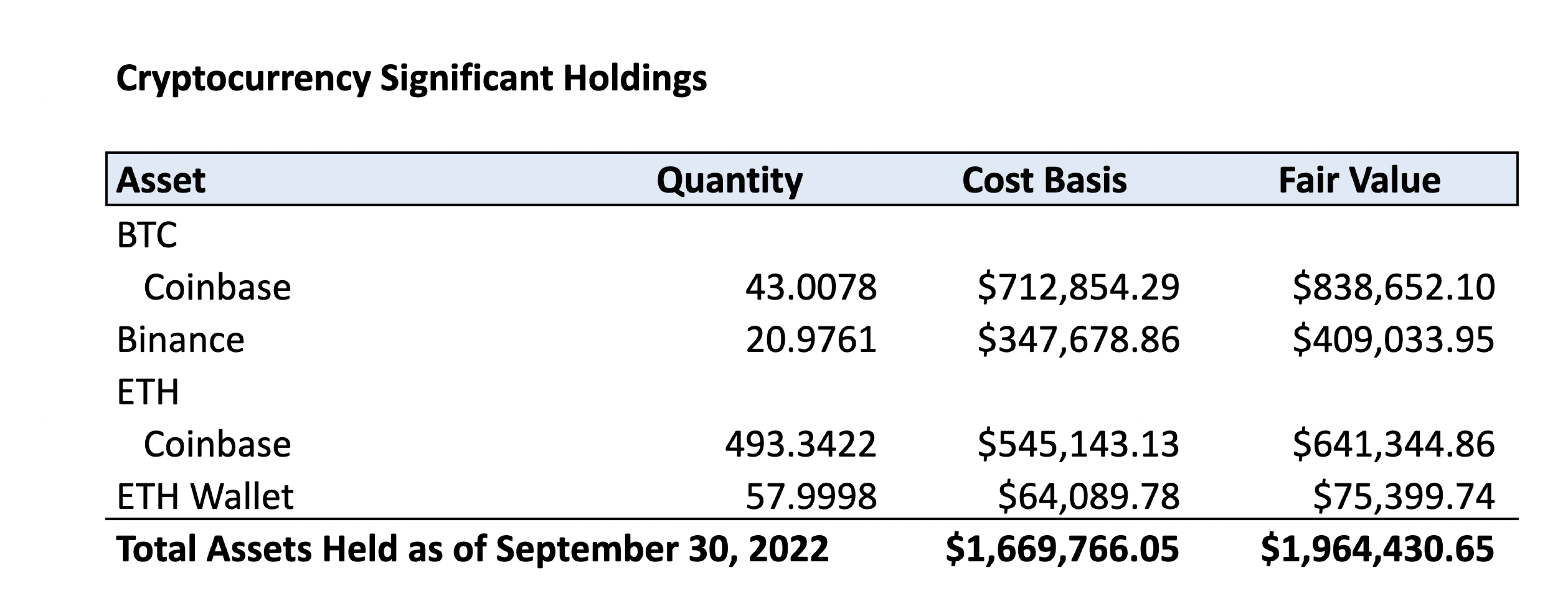

Here is an example of a company’s balance sheet and income statement under the future rules:

In addition to the critical decisions regarding digital asset accounting on balance sheets and income statements, the FASB also made a series of other decisions. Specifically, the FASB clarified how certain cryptocurrency activities should be classified within the statement of cash flows. For example, most cryptocurrency activity would normally be classified under the investing section of the statement of cash flows.

That classification may not be appropriate for companies that receive crypto as revenue and immediately convert those assets to cash – this is especially true for mining companies that immediately sell their mining proceeds. In that case, under the current interpretation, a company would be generating income without classifying the cash generated as part of its operating cash flows.

The FASB clarified that in those cases, it would be more appropriate to classify those cash flows related to asset dispositions as part of the operating section of the statement of cash flows.

The FASB has determined that companies will be required to disclose a series of specific items regarding their crypto holdings and activity:

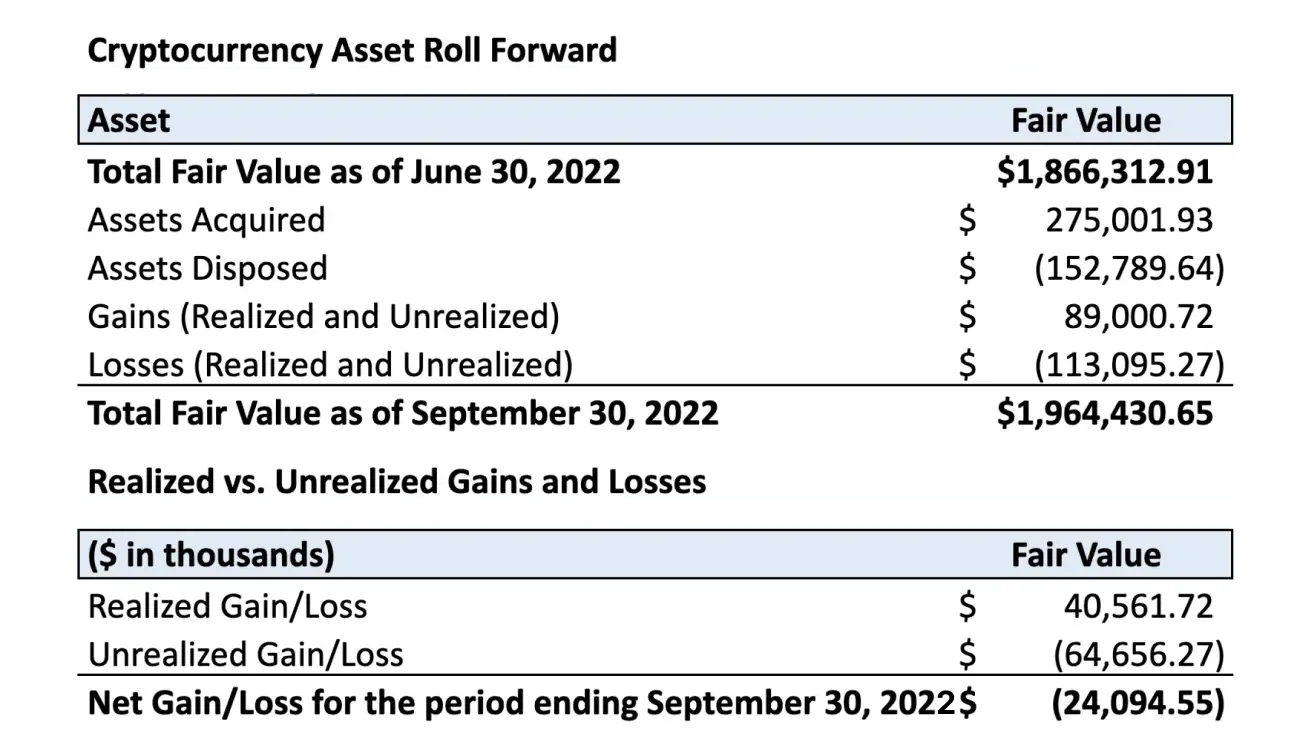

Here are a series of example disclosures based on the FASB’s preliminary decisions:

In addition to these new major disclosures, companies would need to follow existing disclosure requirements outlined in ASC 820, including classifying assets as Level 1, 2, or 3. The Board determined that these will largely be required on a quarterly basis and that these disclosure requirements are applicable to both public and private companies.

While the recent votes are not yet authoritative, in the coming months the FASB will discuss additional provisions related to wrapped tokens and token issuer accounting. In the wake of FTX’s collapse and with regard to accounting for tokens created by a company, this question is more relevant than ever. They will also address transition guidance outlining exactly how and when the new accounting rules should be applied.

Regulatory transparency and better accounting standards can help restore the future of digital assets. Recent and future developments from the FASB will mark critical milestones toward this end. Companies should be preparing for this pending change now to be ready when the official rules are set – likely within the next six months.

At Taxbit, we are building pioneering solutions for digital asset accounting. Our technology is trusted by some of the world’s largest regulatory agencies, accounting firms, and crypto enterprises as we enable the following: